Why compliance matters in fintech and how it drives growth

Nisha Mistry

Compliance in fintech isn’t just about mitigating risk. It’s what enables companies to build trust with bank partners, launch new products, and scale responsibly. The companies that treat compliance as a foundation, not a constraint, are the ones that grow.

When I joined Parafin, we were a small team with a big mission: grow small businesses by giving them access to capital through the platforms they already use. It's a genuinely powerful idea. But building a financial product, one that touches real businesses, bank partners, and money, means that how you build matters just as much as what you build.

That's where compliance comes in.

A lot of people hear "compliance" and picture red tape. Lengthy reviews, legal disclaimers, bureaucratic checklists that slow things down. At a startup, where speed is everything, it can be tempting to treat compliance as something you deal with once you've scaled, once you've raised your next round, or once you have more bandwidth.

I want to make the case for the opposite view. Compliance, done right, is what makes growth possible in the first place.

How compliance builds trust with bank partners

Parafin doesn't operate in a vacuum. We work with bank partners, regulated institutions with reputations to protect, regulators to answer to, and strict expectations for the companies they work with.

When a bank decides to partner with a fintech, such as Parafin, they're extending their own regulatory standing. In return, we bring something they often can't build themselves: technology that moves quickly, underwriting that reaches small businesses traditional credit models miss, and products embedded directly in the platforms merchants already use. It's a real exchange of value, and that's exactly why compliance matters. The relationship only holds if the bank can trust that our speed isn't coming at the cost of their standards.

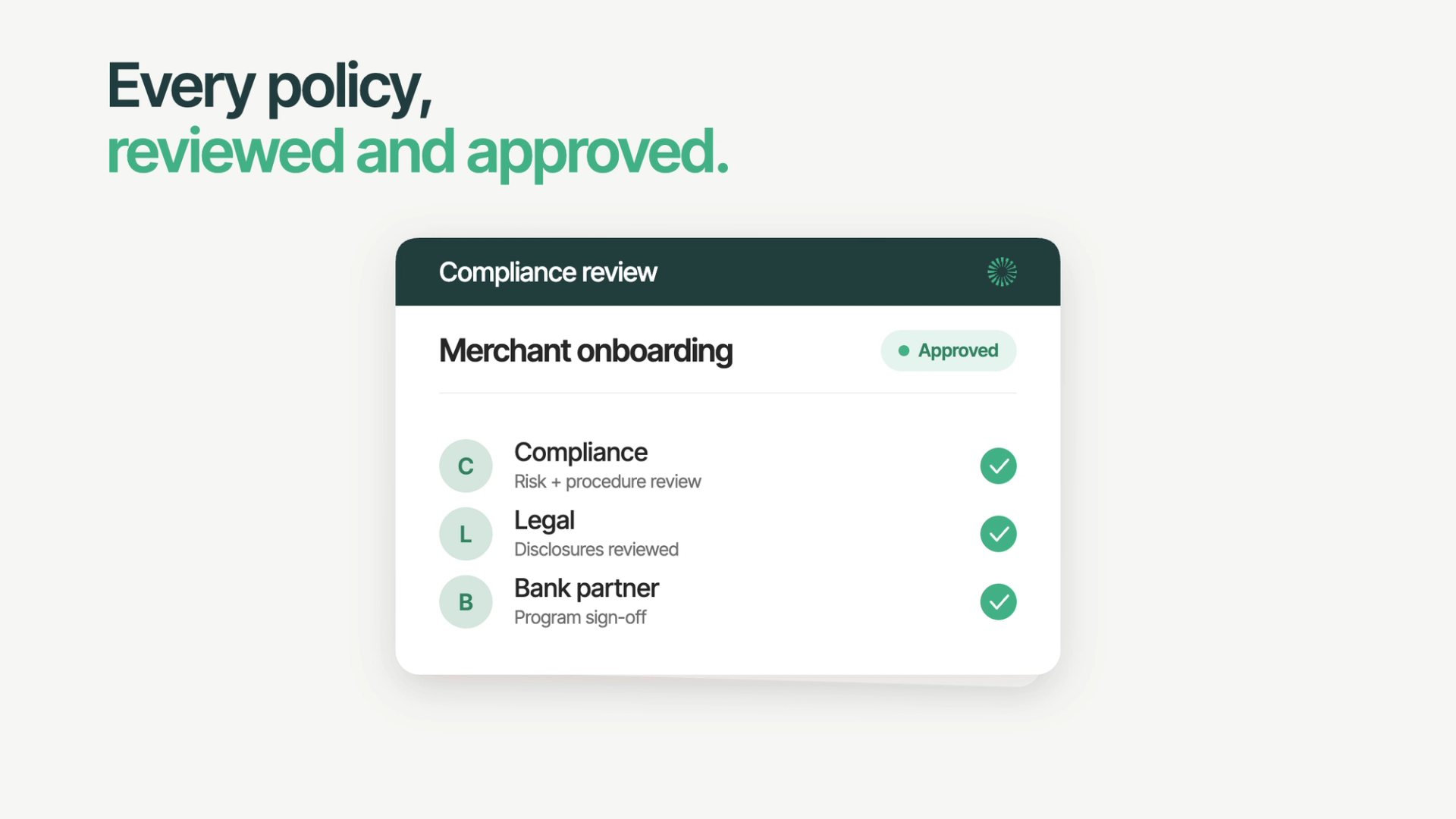

Early on, I learned that compliance isn't just about following rules, but it's about demonstrating to our partners that we take those rules seriously. Every complaint log we maintain, every incident we document, every policy we keep current is a signal: we are the kind of company you can trust.

When something goes wrong, which it inevitably will in financial services organizations operating at scale, the question isn't whether it happened. It's how you respond. Did you catch it? Did you document it honestly? Did you fix it and tell your partners what you found?

That track record is what bank partnerships are built on. And without those partnerships, the product doesn't exist.

How compliance enables growth in fintech

Here's the framing I come back to most often: compliance isn't about saying no. It's about making sure we can keep saying yes.

Every time we evaluate a new product feature, a new partner, or a new merchant population, we're asking: can we do this in a way that's fair, transparent, and legally sound? When the answer is yes, compliance gives the business confidence to move forward. When the answer requires adjustments, compliance is what keeps us from building something that falls apart later.

In fintech, the cost of getting this wrong is high. A simple example is marketing and customer communications. Before something goes live, teams need to make sure the language is accurate, the right disclosures are included, and any required bank review has happened. If that process breaks down, the result can be more than a one-off error. It can lead to audit findings, strain partner relationships, and create reputational risk that is much harder to unwind later.

The startups that scale well in financial services are the ones that treat compliance as a design constraint from the start, not a retrofit.

What it really takes to build compliance from zero

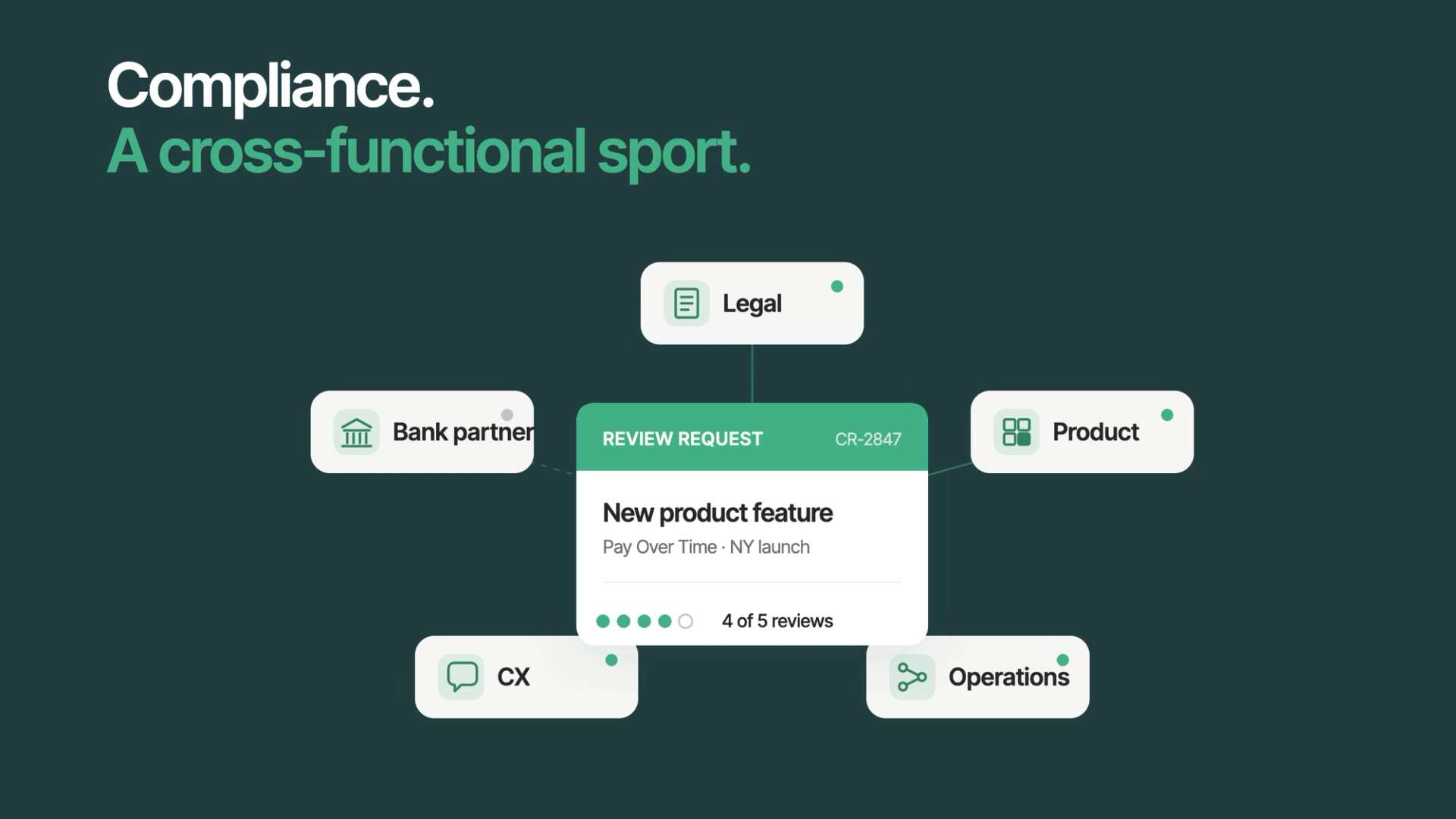

What's unique about joining a compliance function at an early-stage company is that you're not inheriting a system. You're building one.

There's no playbook handed to you on day one. You're writing the policies, designing the review processes, figuring out which regulations apply to which products, and doing it all in real time alongside a team that's moving fast. It requires deep collaboration with Legal, Product, Operations, and Customer Experience because compliance doesn't live in one department. It lives in every decision the company makes.

What I've found is that this is also what makes the work meaningful. You're not just checking boxes. You're shaping how the company thinks about its obligations to merchants, to partners, and to regulators. You're building the muscles that the company will rely on as it grows.

We would also not be where we are today without AI. One example is our exploration of tools that can review marketing content against compliance playbooks and identify potential issues, which helps the team scale parts of the review process more efficiently. That said, compliance still requires humans in the loop to verify outputs and make the final judgment.

The early decisions matter. The frameworks you put in place, the culture of accountability you establish, and the documentation habits you build compound over time. A company that takes compliance seriously at the early stage is in a fundamentally different position at the growth stage than one that doesn't.

Why compliance is a competitive advantage in fintech

The way I see it, in financial services, compliance is a moat.

Regulatory requirements reward companies that invest in strong compliance foundations. The companies that navigate them well with clean audit trails, robust complaint management, clear policies, and strong bank partner relationships, can do things that less compliant competitors can't. They can expand into new products. They can win partnerships with institutions that have high standards. They can weather regulatory scrutiny without operational disruption.

For Parafin specifically, our mission to grow small businesses depends on being a trustworthy infrastructure layer. Merchants trust us with their financial data and their livelihoods. Partners trust us to operate within their regulatory frameworks. The moment that trust erodes, the mission becomes impossible.

Compliance is what keeps that trust intact.

What I'd tell any fintech founder or early employee

Don't wait. Bring compliance into the conversation early, not as a gatekeeper, but as a partner. The best compliance functions don't slow companies down; they help companies move faster with confidence, because they've already thought through the risks.

Build the habits before you need them. Document your decisions. Maintain your policies. Take incidents seriously. Treat your bank partnerships like the long-term relationships they are.

And remember: the goal isn't a perfect compliance program. The goal is a company that takes its obligations seriously, learns from its mistakes, and keeps earning the trust of the people it serves.

That's what makes the mission sustainable. And that's what makes this work matter.