Why we built a true revolving credit card for small businesses, delivered through platforms they trust

Sahill Poddar

A small business owner told us something early on that I keep coming back to.

"During cash crunches, I've thrown things on my personal credit cards, which I hate doing. Sometimes I borrow money from my wife for a few days and pay her back later. Back in the day, I was even pulling stuff from stock accounts."

He runs an automotive repair shop and he's not unusual. More than half of small businesses use personal credit cards to cover business expenses, not because they want to, but because an alternative does not exist.

The average business credit card requires a personal credit score of around 670, which means the business owner is often asked to back business borrowing with personal liability. When they do qualify, the terms are punishing: compounding interest, late fees, limits tied to personal credit history rather than how the business actually performs. Visa estimated at their 2025 Investor Day that over 65 million small businesses in the card issuers' own consumer portfolios have no business credit product at all.

The gap is obvious. The fix is harder.

Our Capital product was the first step: working capital advances underwritten on business performance, not credit scores, for bigger purchases, expansion, and inventory. But capital is a tool for investing in growth.

The more common need is smaller and more frequent, like paying for parts before the customer pays for a job, bridging a vendor invoice, or managing the week-long gap between expense and revenue. Credit cards are already how most small businesses handle this. They’re just using products that weren’t built for business cash flow, with mismatched terms and personal liability attached.

That's what the Parafin Spend Card¹ is built to fix. And doing it right meant building something nobody else in embedded finance has fully tackled: a true revolving credit line.

Why revolving credit is critical, but difficult to offer

When we say "revolving credit line," we mean something specific. A business owner can carry a balance month to month, repay on a schedule that works for their business, and keep spending against their limit. That's how a real credit card works. It's also fundamentally different from the card product that most embedded finance providers offer today.

The more common offering is a card program where the provider supplies program management and infrastructure, but the platform takes on the credit risk and provides the capital itself. Some platforms can extend credit to their customers in the form of a charge card for a limited period, often just a few days, but don’t have the credit expertise or balance sheet to extend beyond that. As a result, businesses are left with a structure where the full balance is due at the end of a short statement period, often with high fees or penalties if it’s not repaid in full, rather than access to a true revolving line.

A true revolving line requires the provider to actually extend credit and hold the risk. That's a much harder thing to build. It means you need:

- Capital to fund outstanding receivables

- Compliance infrastructure to operate a credit program

- Servicing and collections capabilities for when balances roll

And crucially, learning to underwrite well takes years. You need actual credit performance history across multiple borrowing cycles, across different industries and economic conditions, to build a model you can trust. There's no shortcut.

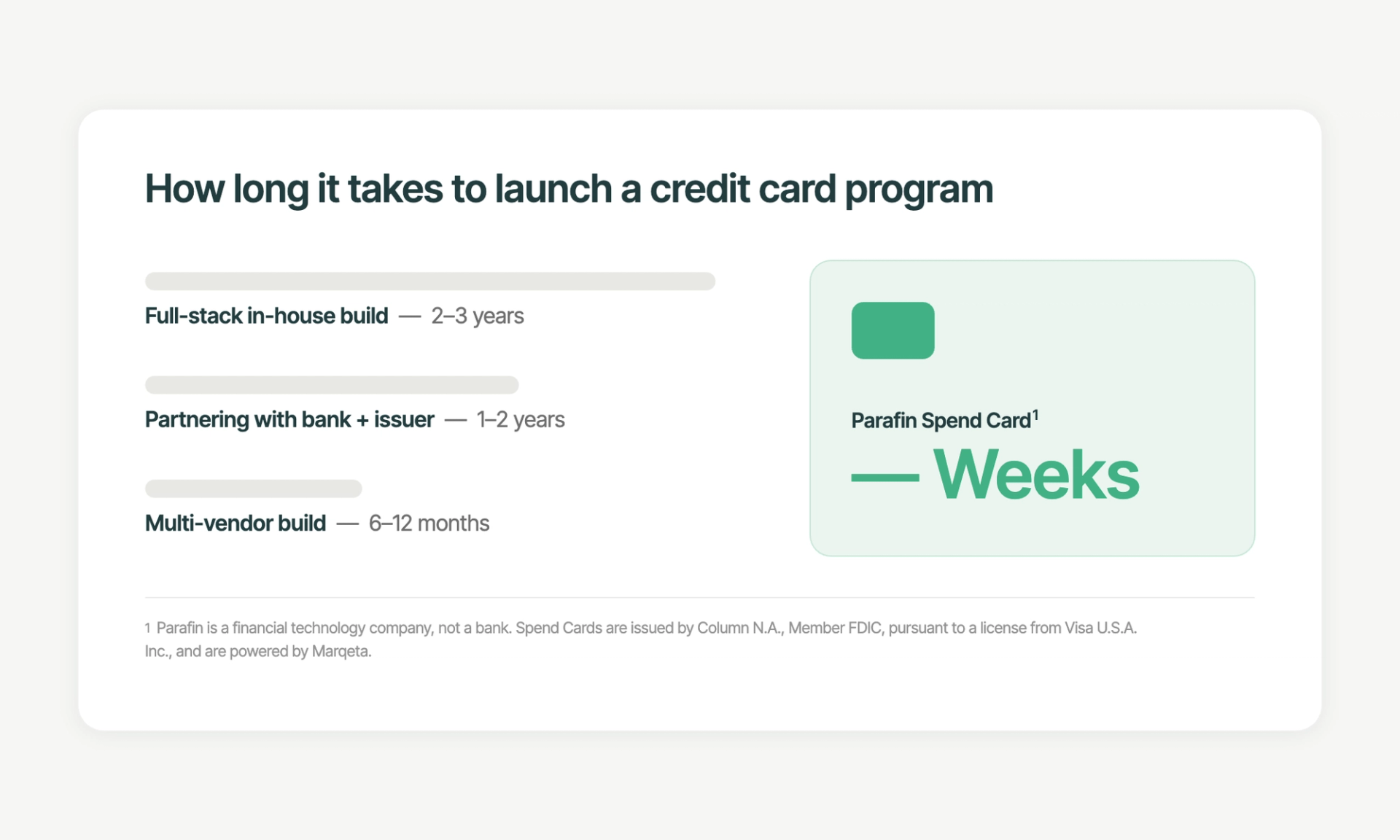

For a platform that wants to offer their business customers a better card experience, assembling all of that is a multi-year, multi-million dollar undertaking and an inefficient use of investment dollars, since it requires building fixed-cost infrastructure (credit teams, compliance programs, capital facilities) that has nothing to do with the platform's core product.

In our experience working with platforms, it can take 6-12 months if you're assembling vendors carefully, 1-2 years if you're directly partnering with a bank, 2-3 years if you're building in-house. And even at the end of that process, most platforms still end up with a charge card or a debit card, because the credit piece is simply too hard to do by themselves.

This isn't hypothetical. Square launched a credit card in 2023 as part of its broader banking expansion, and Shopify has introduced its own credit products. What’s clear from public disclosures is that these programs take time to scale. Even for well-resourced platforms, building a revolving credit product requires establishing performance history, refining underwriting, and growing usage alongside existing lending products.

That's the gap the Spend Card¹ is designed to close. The Spend Card sits on top of a full credit operations stack, built by us so platforms don't have to. And because we take responsibility for the credit risk ourselves, we can offer business customers something the alternatives genuinely cannot: a real revolving line, with balances that can carry over for up to 9 months at a single fee per balance,³ no compounding interest, and no surprises.

Our expertise in SMB underwriting operations

Saying "we take responsibility for the credit risk" only means something if you trust the underwriting behind it. So let's talk about that.

The Spend Card¹ redefines how businesses are evaluated for credit. Instead of looking at personal FICO scores or traditional business credit checks, eligibility is based on actual business metrics: sales patterns, revenue consistency, transaction volume, volatility, expenditure, and existing debt. These are the same signals we’ve trained on across millions of small businesses, funding billions of dollars through our Capital product.

That model is a compounding advantage. Every cohort refines our models that perform across industries, platform, and economic conditions. We have years of credit performance data across a huge range of business types, including how they behave across multiple borrowing cycles. That means better approval rates, better credit sizing, and fewer businesses that fall through the cracks because a personal credit score didn't tell the right story about their performance.

What it translates to for a small business:

- Credit limits tied directly to business performance

- No personal guarantee, no personal or business credit check

- A true revolving line, with balances that can roll over with a single fixed fee³ and no compounding interest

We think this is the right way to underwrite small businesses. And it's only possible because we built the model ourselves and are confident enough in it to support it with our own capital.

What comes with the credit operations stack

The credit is the hard part. But because the Spend Card¹ sits on top of a full credit operations stack, platforms get a lot more than just underwriting when they launch the Spend Card¹.

An experience built around transparency. Pre-approvals mean business owners see their offer before they apply, with transparency throughout the application process. Traditional business credit cards rely on compounding interest, one of the hardest costs for small businesses to predict. The Spend Card¹ is the opposite: no compounding interest and no annual fee. When a business carries a balance, they pay one fixed fee³ and know exactly what they owe and when.

Full platform flexibility. Every Spend Card¹ program is white-labeled under the partner's brand, from the card design to the rewards structure. Platforms can offer cashback rewards⁴ that redeem directly within their ecosystem, keeping spend and engagement inside the platform rather than leaking to a generic card.

One integration for everything. The Spend Card¹ is built on the same data integration as Capital. If a partner is already live with Capital, adding Spend Card¹ requires no new data connection. Same integration, same dashboard, same support structure. A business owner can access a revolving credit line for daily purchases and a working capital advance for bigger growth investments, all through the same platform experience.

Infrastructure built on partners you know. We built this on institutions we trust: Column N.A. for banking and card issuing, Visa for global acceptance, Marqeta for processing and fulfillment. These aren't just vendor relationships — they're the foundation that lets us operate a compliant, reliable credit program at scale. For platforms, that means the operational complexity of running a card program, compliance, disputes, servicing, card fulfillment, and customer support, is handled entirely by Parafin.

What we've seen so far

In early testing, small businesses showed strong interest in the Spend Card¹ with 70% expressing interest in a platform-branded credit card.²

That doesn't surprise us. When you stop making small businesses jump through hoops, no credit checks, no personal guarantee, a fee³ structure they can actually understand, and you meet them inside the platform they already use, adoption follows.

Where we go from here

Spend Card¹ is now live. For platforms like 360 Payments, the Spend Card¹ is a valuable form of business financing for customers on their platform to use in addition to capital. For platforms like Nav, Parafin’s card infrastructure will enable them to extend their 1-day charge card to build business credit into a true revolving credit line. We're continuing to invest in deeper integrations, expanded underwriting inputs, and support for more platform segments.

But more than any specific roadmap item, I want to close on the why.

We started Parafin because we believed small businesses were underserved by the financial system, not because the credit risk was unknowable, but because nobody had built the infrastructure to do it well in the places where small businesses actually operate. Platforms have the distribution. We built the credit operations stack.

The Spend Card¹ is the next step in that. A real revolving credit line, based on business performance, embedded in the platforms small businesses already trust.

If you're a platform thinking about how to bring this to your business customers, we'd love to talk.

¹ Parafin is a financial technology company, not a bank. Spend Cards are issued by Column N.A., Member FDIC, pursuant to a license from Visa U.S.A. Inc. Spend Cards are powered by Marqeta. Approval is not guaranteed and is subject to checks. Terms and conditions apply. See parafin.com/spend for more information regarding the Spend Card.

² Source: Parafin internal analysis of anonymized small business performance data across Parafin-powered programs, 2025.

³ If the full statement balance for a given statement period is unable to be collected by the end of the grace period (i.e., 7 calendar days after the statement period ends), the full statement balance will be rolled over into your pay-over-time balance along with a statement fee of 11%-16% of the statement balance. For more information, please see your Spend Card Agreement.

⁴ Card purchases may be eligible for cashback. See the Rewards Agreement for more information.